: A sophisticated cyber threat")

Digitalization has transformed the way we shop, perform, master and take treatment of our health or travel. Cars and trucks are no extended used just to get from A to B. They are jam-packed with technologies that connects us to the globe, boosts safety, stops breakdowns, and even offers amusement. With the increase of the Net of Matters and synthetic intelligence, a car or truck is no lengthier comprehended entirely in conditions of its effectiveness and smooth structure. It has turn into application on wheels, a gateway to new worlds – not just actual physical, but also digital. And if the character of insurance policy itself is shifting, then the firm providing insurance policies will have to maintain up with these modifications as effectively. Insurance policies requirements digital innovation, as considerably as any other industry area.

These days customers are looking for customization, personalization, and knowledge their wants on an just about natural level. Details and innovative analytics allow us to correctly satisfy these needs. Many thanks to them, it is achievable to fine-tune the provide, not so considerably for a certain team, but for a certain particular person – their behaviors, day by day routine, passions, wellbeing restrictions, or aesthetic choices. And in the case described by us – a person’s driving fashion and commuting patterns.

If you think about it, the insurer has the excellent resource in their fingers. If they can tap into the probable of the computer software-described vehicle and equip it with the appropriate programs, there will be approximately zero probability of inaccurate insurance policy possibility estimates. Information does not lie and shows a factual, not imaginary photograph of a driver’s driving design and actions on the street.

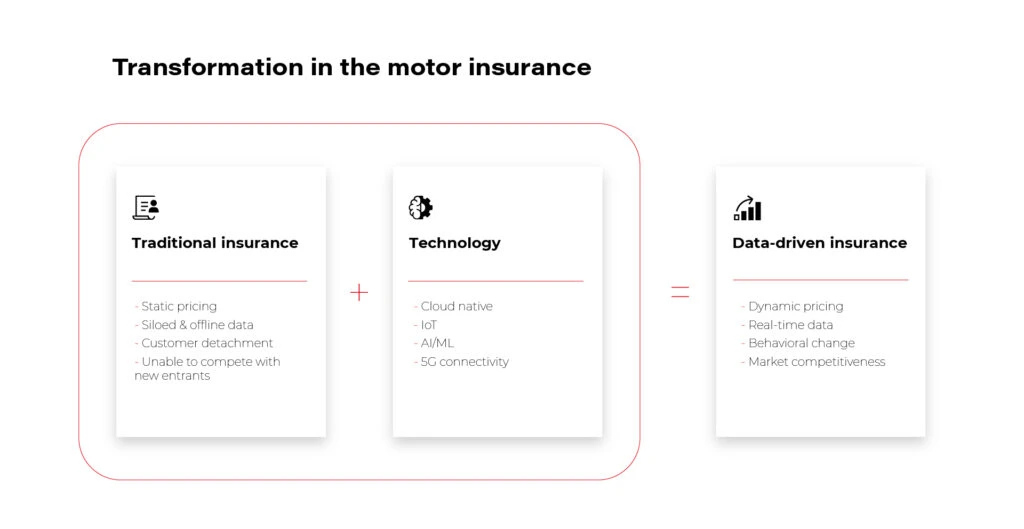

When in the common coverage design pricing is static and facts is gathered offline and not aligned with the driver’s precise tastes, new systems this sort of as the cloud, the IoT, and AI allow for these limits to be efficiently lifted.

With them, an giving is made that competes in the marketplace, generates new income streams inside of the corporation, and builds consumer loyalty.

Data-pushed innovation – simpler said than carried out. Or probably not?

The transformation of a car from a typically understood mechanical product into a “smartphone on 4 wheels,” as Akio Toyoda at the time claimed about modern day autos, will take time and will not transpire right away. But 12 months by calendar year it already occurs, and as the new vehicle products dispersed by the big firms show, this process is truly underway.

Go through our short article on the most up-to-date tendencies in the automotive market

The so-named computer software-described automobile that we are creating with our clients at Grape Up is a auto that moves as a result of an ecosystem of many variables, accessed by distinct gamers and systems.

Plainly, a person these types of supplier can be – and ought to be – the insurance company whose products have been tied to the automotive market place invariably considering that 1897, when a sure Gilbert J. Loomis, a resident of Dayton, Ohio, 1st procured an automotive liability insurance coverage policy.

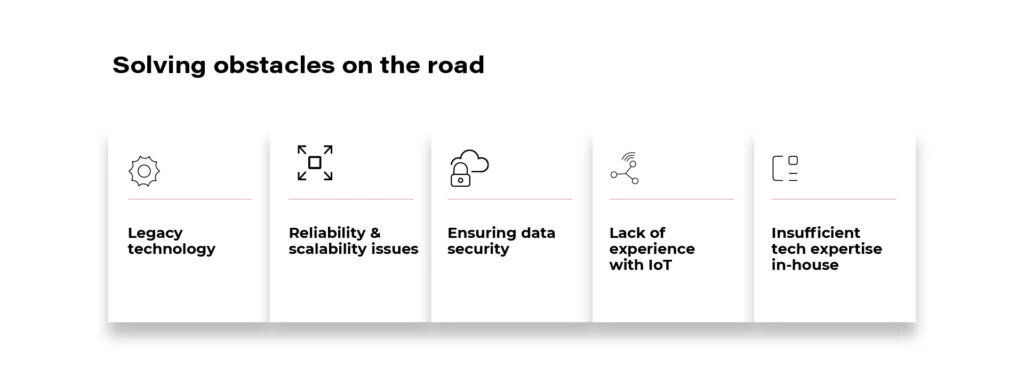

Having said that, for insurance policies providers to perform an integral part in the use of auto-generated info, the driver will have to get a precisely working and protected support from which they will derive true gains. Devoid of constructing precise complex competencies and program-defined vehicle understanding, the insurer are not able to reach these objectives.

Only by creating this kind of business device from scratch in-house, or by partnering with software package firms, will they be equipped to compete with insurtech startups like, e.g. Lemonade, which builds their organizations from the floor up based mostly on AI and knowledge analytics.

The right technologies companion will just take treatment of:

- knowledge security

- selection of cloud and IoT systems

- and will guarantee the reliability and scalability of the proposed answers.

In the course of this time, the insurer can aim on what they do best – establishing insurance policy competencies and tweaking their offers.

How to select the suitable engineering husband or wife?

Just as buyers are looking for coverage that accommodates their driving and life style, an insurance plan business should pick a technology lover that has far more than just specialized skills to provide. Immediately after all, transforming the design in which a standard insurance coverage corporation operates does not boil down to building a digital revenue channel on the Online and launching a fashionable website. We are speaking about a wholly various scale of operations demanding the coverage enterprise to be embedded in a entirely new, rapidly establishing natural environment.

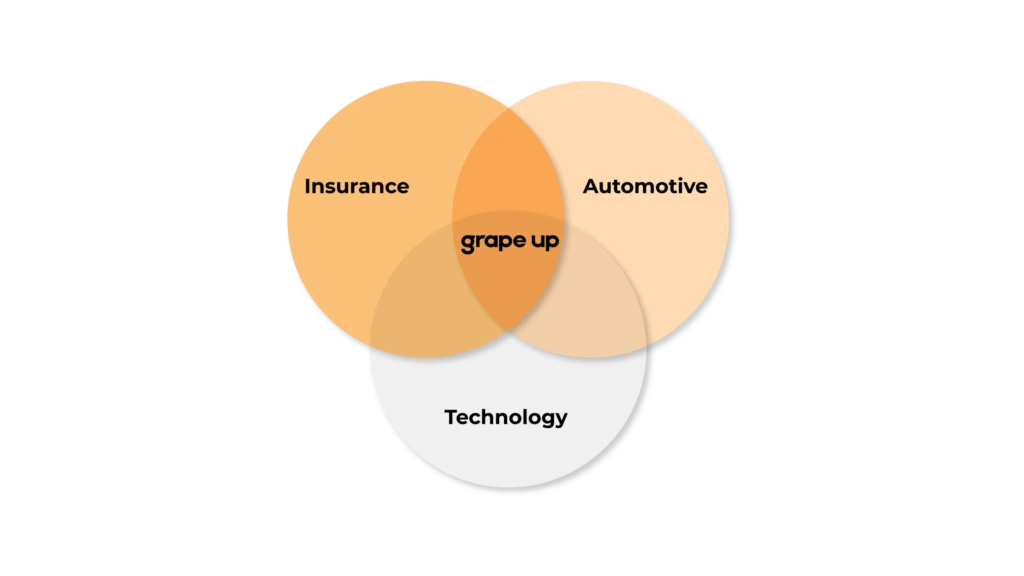

Hence they require a associate who the natural way navigates the software-outlined automobile ecosystem, understands its details, and has knowledge in doing work with the automotive business. In addition to, it must be anyone educated about the specifics of the P&C coverage current market and the worries confronted by the coverage customer.

It is only at the intersection of these a few locations: technological innovation, automotive, and insurance policy, that competencies are designed to efficiently compete from modern day insurtechs.

Like in the Japanese philosophy of ikigai, which points out how to find one’s feeling of reason and give which means to one’s work, equally firms can establish worthwhile, practical options for buyers. They will convey pleasure not only to buyers but also to the insurance policy corporation, which will open a new revenue channel and meet up with the requires of the current market.